When Silence Costs Lakhs: Contesting a Tax Demand Born from an Unseen Notice

If no opportunity to reply or be heard was given, the order is invalid for violating natural justice and the bank attachment should be lifted.

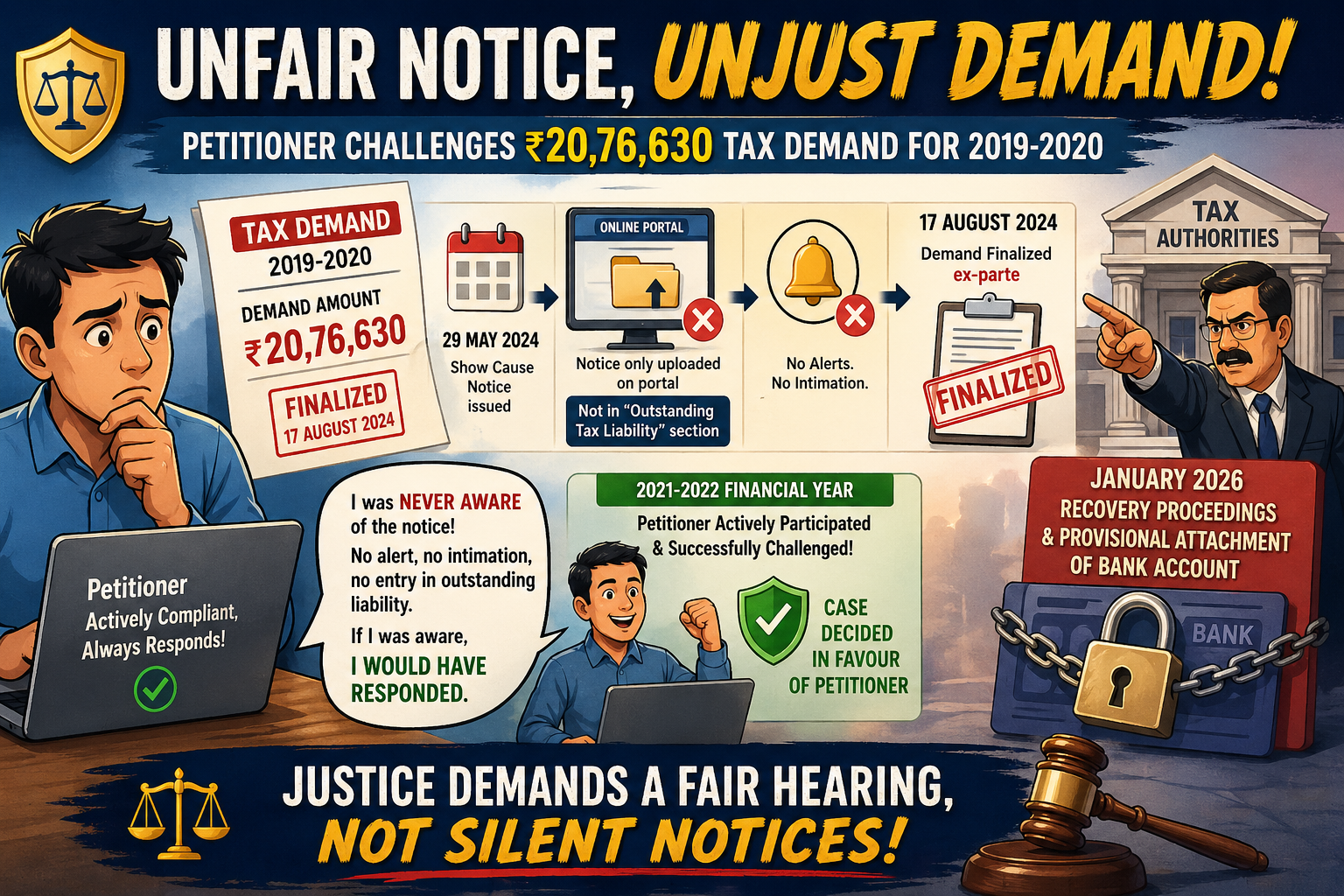

Facts of the case

The petitioner is challenging a tax demand of ₹20,76,630 for the 2019-2020 financial year, which was finalized on August 17, 2024, after they failed to respond to a show cause notice issued on May 29, 2024. Following this, tax authorities initiated recovery proceedings and provisionally attached the petitioner’s bank account in January 2026. The petitioner argues that they were never aware of the original notice because it was only uploaded to the online portal without appearing in the “outstanding tax liability” section or triggering any alerts, and they point to their active participation in a separate, successful challenge for the 2021-2022 financial year as proof that they would have responded to this notice as well had they known about it.

Issue of the case

Whether the Order-in-Original should be set aside due to a violation of the principles of natural justice specifically, the petitioner’s lack of opportunity to file a reply or attend a personal hearing and whether the resulting bank account attachment should be lifted?

Taxpayer Wins: Tribunal Slams Unnecessary Re-investigation After Source of Funds Was Already Proven

Decision of the Court

The High Court has set aside the original demand order and ordered a fresh review of the case, ensuring the petitioner gets a fair chance to present their side through a formal reply and an in-person hearing. To proceed with this new adjudication, the petitioner must first deposit the full disputed amount of ₹20,76,630, though the court has ordered the immediate lifting of the bank account attachment. Additionally, the petitioner must pay costs totaling ₹50,000 to the local Bar and Clerk Associations and is required to appear before the tax authorities on April 30, 2026, to begin the process.