ITO’s Rejection of Books and 8% Profit Estimation Requires Fresh Appellate Examination; ITAT Remands Matter to CIT(A)

ITO’s Rejection of Books and 8% Profit Estimation Requires Fresh Appellate Examination; ITAT Remands Matter to CIT(A)

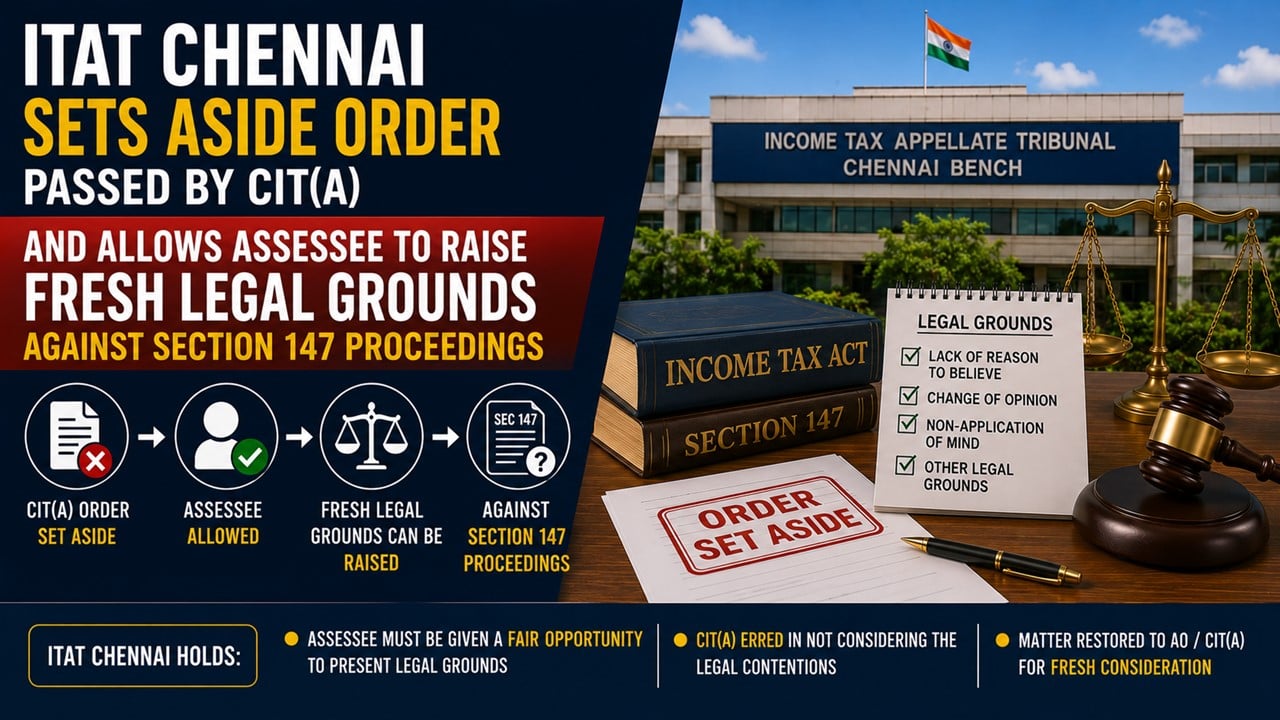

The Income Tax Appellate Tribunal (ITAT) Chennai set aside the order passed by the CIT(A) to decide the appeal afresh in accordance with law after providing an adequate opportunity of hearing to the assessee.

The assessee is an individual engaged in the business of purchase and sale of paddy through the proprietary concern named V. Gowri Traders and had not filed her return of income for assessment year 2018-19 and according to the information available with the Department regarding cash deposits amounting to Rs.72.45 lakh and cash withdrawals aggregating to Rs.3.04 crore, the AO initiated proceedings under Sections 147 and 148 of the Income Tax Act, 1961.

Govt Increases Special Additional Excise Duty on Diesel from Rs 13.5 per Litre to Rs 14 per Litre

In response to the notice issued under Section 148, the assessee filed a return declaring a total income of Rs 5.56 lakh and explained that the cash withdrawals were utilised for making payments to small farmers from whom paddy was procured. However, the assessee failed to furnish complete books of account and supporting documents.

The AO invoked Section 145 and estimated income by applying a net profit rate of 8% on the disclosed turnover of Rs 2.48 crore. Aggrieved by the assessment order, the assessee preferred an appeal before the CIT(A), which confirmed the additions made by the AO.

The Tribunal observed that although the assessee had failed to properly present the appeal before the CIT(A), ordinarily an assessee should be afforded an effective opportunity to substantiate the case. The Bench further noted that adjudication of issues on merits requires an examination of facts and records and the Tribunal considered it appropriate to restore the matter to the file of the CIT(A).

Accordingly, the impugned order was set aside and the appeal of the assessee was allowed for statistical purposes.